Warnings of rising consumer debt useless for consumers

The FCA's chief executive Andrew Bailey said that increasing levels of debt were partly a result of a greater generational shift in wealth towards older generations, and warned both customers and banks alike that credit should be "affordable".

His remarks come at a time when new figures from PricewaterhouseCoopers predict that the total amount of unsecured debt will come to £340 billion - or £12,500 per household - by 2020.

Yet as much as warnings on consumer debt are backed up by rising figures, the fact that such debt is being driven by high living costs and low wage growth underlines how, regardless of any well-meaning pronouncements on the part of officials, it will inevitably continue rising for as long as such conditions prevail.

£300 billion

Andrew Bailey's warnings also coincide with a new survey from PricewaterhouseCoopers (PwC), who discovered that unsecured lending has reached an all-time high of £300 billion.

This sum includes borrowing on credit cards, student loans, overdrafts and personal contract purchases (PCPs) for cars, and it grew by 11% in the past year: the fastest rate since 2002.

This equates to £11,000 per household in the UK, and what makes it particularly alarming is that, according to PwC, "total levels of unsecured personal debt are now 30% higher than their pre- financial crisis peak".

This chimes in with warnings made by the Bank of England as far back as last November, yet another alarming facet of the rise in debt is its disproportionate impact on younger individuals and households.

As PwC explain, people aged between 25 and 34 hold five times as much debt on average as those aged 55 or over. Making matters worse, renters - who generally younger rather than older - are nearly twice as likely than homeowners to have to pay for essential household items by going into debt.

Pushing debt onto the young

And this is precisely what Andrew Bailey has warned of in a new interview, explaining, "There has been a clear shift in the generational pattern of wealth and income, and that translates into a greater indebtedness at a younger age".

He referred to how the FCA is looking at measures to ease problem and persistent debt, adding, "There are particular concentrations [of debt] in society, and those concentrations are particularly exposed to some of the forms and practices of high cost debt which we are currently looking at very closely because there are things in there that we don't like".

His concerns have been picked up by other parties recently, with the Labour Party calling last month for a cap on the amount of interest payable on a credit card.

They want to limit it to 100% of what was spent on a card (e.g. the card's balance), thereby ensuring that people avoid racking up oversized debts.

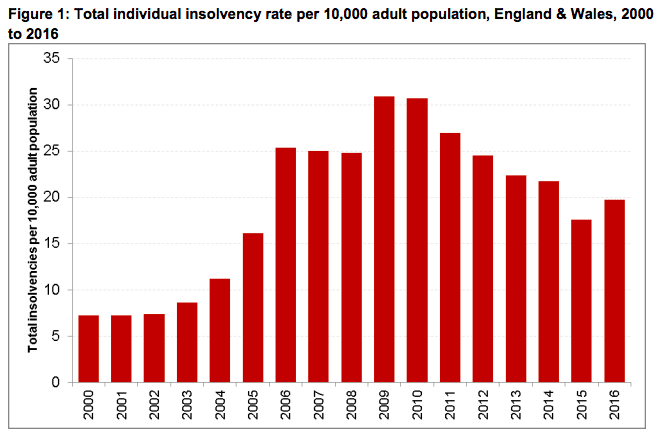

That this would be at least a timely measure is also supported by the latest data from the Insolvency Service. They revealed that personal insolvencies grew by 16%, after a period of decline following the financial crisis.

Source: Insolvency Service, Individual Insolvencies by Location, Age and Gender,

England and Wales, 2016

Inflation and wage growth

However, as serious as the issue of rising debt undoubtedly is, simply warning against it - as Andrew Bailey, the Bank of England and others have done - isn't enough.

As Bailey himself admits, debt isn't rising because people are becoming increasingly irresponsible and impulsive. He said, "We should not think this is reckless borrowing, this is directed at essential living costs".

In other words, people are borrowing simply because, with inflation now hitting 3% and wage growth at 2.1%, they have no other way of surviving.

As such, simply pointing out that an interest rate hike is on its way will have no effect, since it won't change the fact that too many people are unable to pay their living costs except by borrowing.

And it's likely that, with demand for credit so high, measures to limit debt will be ineffective.

To take only one possible measure, while Labour's proposed interest cap will stop interest charges on a single credit card from rising too high, it won't stop customers from applying for additional cards from other lenders, and neither will it stop lenders from providing them.

As a result, the only effective way of halting the growth in debt is to accelerate the growth in wages, to tame housing costs by building more accommodation, and to keep inflation down by increasing the UK's economic performance and prospects.

Yet with Brexit negotiations still up in the air, it may be some time before the UK is able to achieve this.

We are independent of all of the products and services we compare.

We order our comparison tables by price or feature and never by referral revenue.

We donate at least 5% of our profits to charity, and we aim to be climate positive.

Latest News

26 October 2022

Cost of living showing worrying trends in affordability

16 June 2022

FCA warn lenders on cost of living difficulties