Debt repayment: the options available

When and where to get help

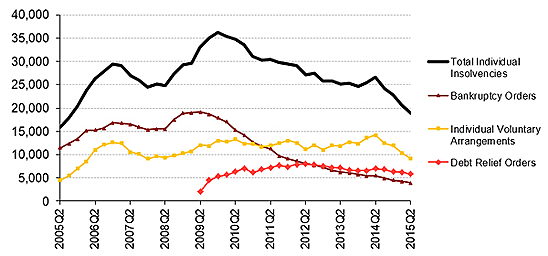

Personal insolvency figures lowest since recession

Credit: Jinga/Shutterstock.com

Between April and June this year, 18,866 people became insolvent in England and Wales.

That's a fall of more than 29% on the same period last year, and the lowest figure for a decade.

Types of insolvency

Insolvency describes three legally binding, or "formal", forms of debt relief: Debt Relief Orders (DROs), Individual Voluntary Arrangements (IVAs), and bankruptcy.

A DRO typically helps people who have few assets and a relatively low level of debt; an IVA allows people to make reduced payment over five or six years, after which the rest of the debt is written off.

Bankruptcy is the most drastic measure, reserved for those who need to write off debt they have no realistic chance of ever repaying.

Approximately half (48%) of people facing insolvency opted for an IVA between April and June 2015, according to Government statistics [pdf].

By comparison, 31% used Debt Relief Orders, and 21% became bankrupt.

SOURCE: The Insolvency Service. Available here [pdf]

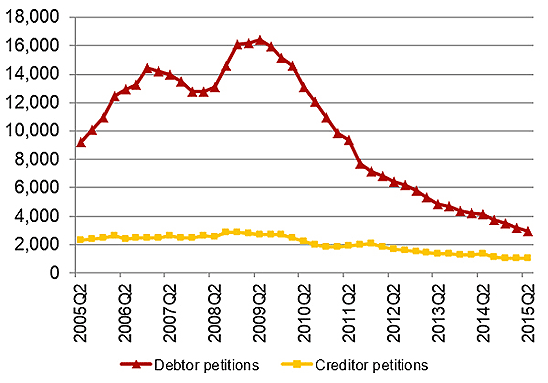

Bye bye bankruptcy?

It's welcome news that the number of people filing for bankruptcy is at its lowest level since 1990. Bankruptcy is, after all, the most punishing form of debt relief, and has implications that last for years.

We can also expect to see a further decline in these numbers under new rules that increase the threshold at which creditors can push for someone to be declared bankrupt.

At the moment, people can be forced into bankruptcy if they owe just £750. The Government will increase this to £5,000, by the end of October 2015.

At the same time, the maximum debt covered by DROs - a relatively low cost alternative - will be increased from £15,000 to £20,000.

SOURCE: The Insolvency Service. Available here [pdf]

DMPs - the silent partner

Useful Information

The Insolvency Service's latest figures consider the three legally binding routes out of insolvency, but this isn't really the full picture.

It's estimated that hundreds of thousands of people are struggling out of debt using Debt Management Plans (DMPs). These are informal agreements between debtors and creditors, normally arranged by a third party debt management company.

The person who owes the money makes a fixed monthly payment to the debt management company, who then divides it amongst the creditors.

Although they've been around since the 1990s, DMPs have recently come under fire from the Financial Conduct Authority.

As a result of the increased scrutiny, it's expected that the number of debt management companies in operation is going to fall, leaving people looking for alternate ways out of debt.

"Free" DMPs, arranged by charities and other social organisations, will still be available, but it remains to be seen how the decline in the number of avenues available to people will affect the number of IVAs, DROs and bankruptcies.

Tread cautiously

Another reason to be cautious about the Insolvency Service figures is that they say little about the future.

This won't be helped by national cuts to tax credits. The Government is aiming to shave around £12 billion from the welfare budget, which some say will result in £1,000 a year cuts for three million families.

At the same time, alarm bells are starting to sound among debt specialists who worry that we're enjoying ourselves a little too much right now.

The Bank of England have said that interest rates will begin to rise at "the turn of the year", and will continue to rise over the next three years.

A recent report from Moody's says that more of us are using credit cards to cover the costs of yesterday and today, without thinking about how or when we're going to pay it all back.

And Jane Tully of the Money Advice Trust warns that we're ill prepared for the imminent rise in living expenses.

"Household debt is forecast to pass its pre-recession peak of 169% of household incomes in 2020," she says. "We are concerned that many will turn to credit to plug gaps in their budgets.".

We are independent of all of the products and services we compare.

We order our comparison tables by price or feature and never by referral revenue.

We donate at least 5% of our profits to charity, and we aim to be climate positive.

Latest News

26 October 2022

Cost of living showing worrying trends in affordability

16 June 2022

FCA warn lenders on cost of living difficulties