Credit cards bounce back - but is that good?

Their figures for October 2014 show the number of purchases made on credit cards was up 8% from the same time in 2013.

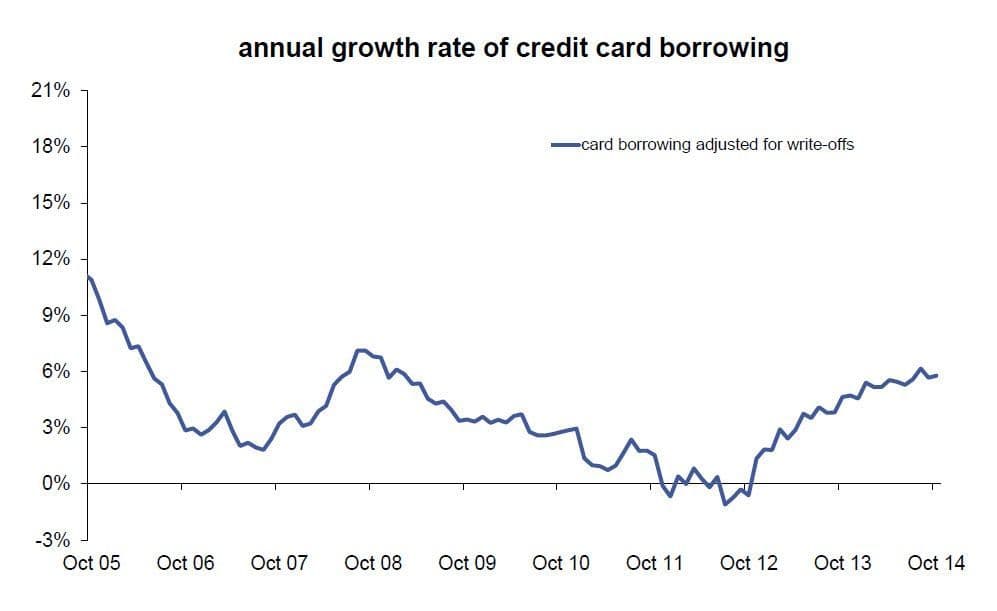

The rate of growth in credit card borrowing has also risen to 5.8% annually, a slight increase on the rate of growth a month earlier.

Nearly 42% of borrowing is interest-free, as customers take advantage of stiff competition in the 0% balance transfer market, and extended introductory periods.

But while the BBA hails all this as a sign of increased consumer confidence, could it also be the case that more of us are using whatever option we can to meet day-to-day costs?

SOURCE: BBA Credit Card Market - October 2014

Credit, crunched

The number of credit cards in circulation reached a low in 2011. The amount we spent on them reached a low point in 2012.

Since then, both have been steadily rising again, to the point that the UK now has a total of £58.9 billion in outstanding credit card debt - the highest for three years - and that there are 60 million credit cards in circulation, attached to 51 million credit accounts.

In October alone there were 218 million credit card purchases worth some £12.5 billion.

The BBA say 66% of credit card accounts had an outstanding balance at the end of the month - which equates to an average of £1,750 owed on each card.

Of course it doesn't break down like that, as Citizens Advice say the people who come to them for help with serious debt owe an average of £6,000, and StepChange say their clients have average credit card debts of more than £9,000.

Meanwhile interest rates have been steadily creeping up since 2009.

As credit card companies make the majority of their money from interest charges, all those 0% deals are being paid for - and then some - by the 58% of borrowing that is subject to interest.

Putting off the inevitable

It's true that the economy does seem to be picking up, but for many people wages haven't increased anywhere near enough - if at all - to keep up with the rising cost of living.

Instead, research for the FCA suggests that most of us "resist" taking out credit cards for as long as possible, only giving in and applying after being worn down by marketing pressure.

Further to this, many card holders report becoming reliant on their plastic to support their everyday spending.

And given the time of year, it's likely many people are facing bigger bills and large one-off purchases.

So it comes as little surprise that the Money Advice Service (MAS) says almost 46% of people expect to cover the cost of Christmas 2014 with their overdraft or credit card - up from 32% in 2013.

At the same time, they say the proportion of us finding it difficult to pay for it all, or worrying about where to find the funds, has dropped.

With so many more credit cards in circulation, it's entirely possible many people are buying today and putting off paying, or at least spreading the pain, for as long as possible.

T's and C's apply

The problem with that, though, is that many of us are optimistic in entirely the wrong way.

One in three people who take out a credit card with a 0% balance transfer offer won't repay it within the interest free 0% period.

As we reported at the time, one in five balance transfer holders have their 0% deal ended early by their card provider for breaking the terms and conditions of the offer - most for being late with, or completely missing, a monthly payment.

With continuing job uncertainty and a move towards tighter affordability checks for new applicants, many people have found themselves paying more than they predicted on cards they now find it difficult to swap away from.

There's no one factor behind the rise in the number of credit cards, or the amount we're spending on them - but the BBA's optimism about increased borrowing isn't something many of us will share.

We are independent of all of the products and services we compare.

We order our comparison tables by price or feature and never by referral revenue.

We donate at least 5% of our profits to charity, and we aim to be climate positive.

Latest News

26 October 2022

Cost of living showing worrying trends in affordability

16 June 2022

FCA warn lenders on cost of living difficulties