How credit card optimism costs us money

Figures released by Consumer Intelligence show that one in three of those that take out a credit card balance transfer won't repay it within the 0% period.

Cardholders' optimism about how much they'll be able to pay has very real effects: not only have they paid transfer fees for the new card, they're opening themselves up to high interest charges.

Behavioural Economists call the difficulties we have in predicting future behaviour projection bias.

This optimism about the future persists even as real evidence to the contrary, like past experiences, stacks up, researchers have found.

"Any attempt to change risk perceptions is hampered by the variety of strategies individuals can use to arrive at optimistic conclusions," one 1995 study attempting to identify 'de-biasing' strategies concluded.

Another important study, Making Credit Safer written by current US senator Elizabeth Warren and her colleague Oren Bar-Gill, has noted that, "at the time they take out their cards, consumers are optimistic about their future credit needs, about their future willpower, about the likelihood that they will switch to a new card with a new, low introductory rate, or about all of the above."

In the specific case of balance transfers, projection bias could be manifesting itself in the inability to foresee events which will prevent sufficient payments being made to clear the debt within the 0% period or an unwillingness to recognise that personal behaviour, an inclination towards disorganisation, for example, will likely lead to being unable to repay in time, as it may have in the past.

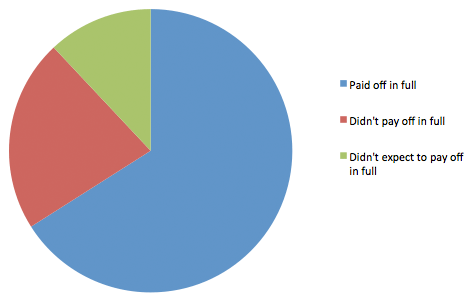

As shown in the chart below, Consumer Intelligence found that 34% of those with balance transfers had either failed to repay within the 0% period or, in 12% of cases, expected that they wouldn't repay their current balance within the 0% period.

Balance transfer users that repaid within the 0% period. Source: Choose, from Consumer Intelligence data.

Previous research into balance transfers has found exactly the same pattern: about a third of cardholders end up paying interest on their interest free deal.

Curing Pollyannas

If projection bias is behind cardholders' inability to repay their total balance within the promotional 0% period, how can we cure them of their optimism?

Or, to put it perhaps a bit less emotively, as researchers in this subject do, how could consumers become de-biased and see their choices more clearly?

One solution might be more information when consumers consider new borrowing but, because of the way this bias works, its effects seem likely to be minimal.

Researchers into optimism find that we tend towards exceptionalism.

In one classic study, for example, people rated their own driving as much better than the average, even when asked to consider statistics on accidents before answering.

Some researchers, for example, Jason West in a 2012 study, have suggested that deeper changes to the way information is presented, for example, including a test for consumers on affordability before they can take a product, might make more of a difference.

It's worth noting at this point, however, that the effect of more sophisticated consumers in the balance transfer market might well be the market ceasing to exist.

While card providers do make money from all their balance transfer customers, through upfront fees, it is the interest payments made by overly optimistic customers switching large balances to the providers that allows them to offer 0% deals at all. By most estimates, about 65% of credit card provider profits come from interest payments.

Sophisticated consumers profit from the minority paying interest.

When optimism isn't to blame

In addition, if efforts to de-bias consumers are going to be successful, however, researchers should first determine if projection bias is indeed to blame when cardholders end up paying interest.

For example, decisions that look illogical from the outside, or from a researcher's overhead point of view, may actually be totally logical from the point of view of the consumer.

Again, we can see this clearly in the balance transfer market.

Up until a few years ago, not clearing the balance within a 0% period, as long as you planned on rolling the debt over to another 0% balance transfer deal, was regarded as a pretty savvy move.

That has changed as credit card acceptance rates have plummeted.

"A lot of [cardholders] may try to roll over to another 0% deal and they may or may not be available," David Black of Consumer Intelligence said, speaking on BBC Breakfast about this week's survey results.

If consumers do not plan to roll over their balance in this way, however, their behaviour is pretty illogical.

As we have shown here, eventually paying a balance transfer deal off after the introductory rate has expired is highly likely to be more expensive than just leaving it where it was and will certainly be more expensive than moving it to a low interest rate card instead.

Even if they do plan to move to another deal, however, they are just optimistic in a different way, they think they'll be able to get another 0% deal, but it's worth considering that they may be right: there are certainly plenty of offers on the market.

Again, though, the evidence suggest that most won't or won't be able to move.

In addition, there is another indicator that more strongly suggests that those paying interest on a 0% deal have made a mistake.

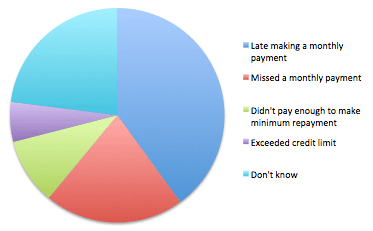

One in five balance transfer holders see their 0% deal ended early by the provider for breaking the offer terms and conditions.

Reasons that a 0% period was terminated.

Source: Choose, from Consumer Intelligence data.

One study from 2004, when credit was more widely available, found that a majority of credit cardholders didn't switch again once introductory deals were over.

As the chart to the right shows, most of them, 40%, were late making a monthly payment.

Another 21% missed a payment entirely, 10% paid less than they were meant to, 6% exceeded the card's credit limit and it's probably safe to assume that the 23% who didn't know why they lost their 0% rate also fell into one of those categories.

Looking on the bright side...

In her book The Optimism Bias Tali Sharot notes that, in general, optimists work longer hours and tend to earn more.

Economists at Duke University have found that optimists tend to save more.

As we look down the barrel of Christmas spending this year, however, it might be worth considering how far it is realistic to expect to repay money borrowed for all those presents.

New Years resolutions are, after all, a great example of misplaced optimism.

We are independent of all of the products and services we compare.

We order our comparison tables by price or feature and never by referral revenue.

We donate at least 5% of our profits to charity, and we aim to be climate positive.

Latest News

26 October 2022

Cost of living showing worrying trends in affordability

16 June 2022

FCA warn lenders on cost of living difficulties