Fee free transfers guide

Unofficial transfers guide

Poor credit and transfers learn more

Why fees are the new balance transfer battleground

Credit: one photo/Shutterstock.com

38% of balance transfer credit cards are currently offering fee promotions, some reducing the cost of moving a balance to as little as 0.75%, research carried out by this site found.

Although 0% balance transfer periods have also increased in the past few years, the top deal is currently 31 months, the rash of fee promotions that have hit the market recently show that providers are looking beyond long promotional periods to attract different kinds of customers.

More on balance transfers

Low fees are typically offered with credit cards that have fairly short interest free periods which makes them particularly attractive to those looking to pay off a card balance of just a few hundred pounds using a 0% deal.

Fee deals in fashion

We looked at 39 balance transfer credit cards and found that 14, about 38%, had promotional fee offers.

Three more credit cards are offering low balance transfer fees, 1.5% or lower, as standard.

It was interesting to see, however, that although a lot of cards were offering fee reductions they weren't always offering very low fees as a result.

Some Barclaycard credit cards are offering promotional fees of between 2.45% and 2.99%, for example, about average for any card on the market.

In contrast, when we did our research Nationwide were offering a fee promotion which reduced the upfront fee to just 0.75%, the lowest fee ever offered in the UK.

As you can see below, that makes a big difference.

| Balance to move | 0.75% fee | 1.5% fee | 2.45% fee | 3% fee |

|---|---|---|---|---|

| £500 | £3.75 | £7.50 | £12.25 | £15 |

| £1,500 | £11.25 | £27.50 | £36.75 | £45 |

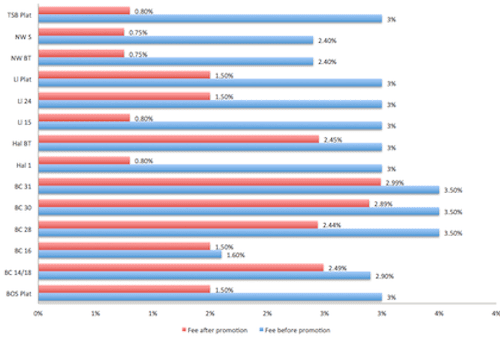

In addition, some promotions were more generous with their reductions than others.

As you can see in the chart below, while most deals reduced fees by at least 50%, one lowered the fee by just 0.1%.

Balance transfer fees before and after promotions

SOURCE: Choose research carried out March 2014.

The downside of fee promotions

That's one downside to fee promotions: credit card providers can use them to make a deal look more attractive, even though their fee is just average; it's the supermarket promotion approach to balance transfers.

Another is that these promotions are often tied to shorter 0% periods.

That can be a good thing, especially for those with a small balance, but it could also push people to take a shorter 0% deal that might not be suitable.

We've previously covered research showing that many credit cardholders end up paying when they take 0% deals as a result of an 'optimism bias' that makes them likely to believe they'll be able to repay quickly.

Millions of balance transfer customers end up paying interest, even though they moved their balance specifically to avoid it.

Natwest and RBS recently stopped offering 0% promotions altogether for this reason.

The banks said that interest free deals were luring consumers into 'debt traps' and that cardholders who were able to use the deals successfully - that is, repay their debts within the 0% period - were only able to profit because so many customers end up losing out when they take these deals.

Card providers fight for new customers

Whether or not they're always suitable, the rise in the number of balance transfer fee promotions is a sign of an increasingly competitive market for balance transfers.

Moneyfacts research released last year found that the best balance transfer deal in 2010 was 16 months long.

Today that's almost doubled: the longest is 31 months interest free.

Longer interest free promotions can become unprofitable for card providers, however, which may be why so many are turning their attention to balance transfer fees.

Fee promotions also allow card providers to attract different kinds of customers, those with fairly small credit card debts who might not otherwise have considered taking out a new card in order to pay down the debt.

We are independent of all of the products and services we compare.

We order our comparison tables by price or feature and never by referral revenue.

We donate at least 5% of our profits to charity, and we aim to be climate positive.

Latest News

26 October 2022

Cost of living showing worrying trends in affordability

16 June 2022

FCA warn lenders on cost of living difficulties