How to stooze money out of your card

How to use balance transfer cards

Can I transfer to a current account?

0% vs life-of-balance transfers

Card spending grows as lenders reduce 0% interest deals

Credit: Nattakorn_Maneerat/Shutterstock.com

According to research carried out by Moneyfacts, the number of 0% introductory balance transfer deals on the market has decreased from 126 to 119 in six months, while the longest period being offered by a 0% deal has shrunk from 43 to 40 months.

This comes at a time when spending on credit cards grew by 6.9% in the 12 months to June, and when savings grew at only 2.3% in July, the lowest rate for eight years.

Yet while it might seem that generous balance transfer deals are being slowly withdrawn to counter the economic risk posed by high borrowing, the reduction in deals is still too small to confirm an emerging trend, while credit card borrowing hasn't in fact grown as fast for most of 2017 as it has in previous years.

Credit card spending

Relevant guides

That said, spending on credit cards has been growing steadily over recent months, an issue that was flagged up at least as early as late November, when the Bank of England issued a warning on the high level of debt households have been accumulating.

Since then the problem seems only to have worsened, with the following table showing how spending on credit cards has grown since the beginning of the year.

| Month | Growth rate in spending value | Growth rate in number of transactions |

|---|---|---|

| Jan | 3.3% | 7.6% |

| Feb | 4.1% | 8.2% |

| Mar | 5% | 8.8% |

| Apr | 5.7% | 9% |

| May | 6.4% | 9.2% |

| Jun | 6.9% | 9.3% |

Source: UK Finance, Card Expenditure Statistics, 2017

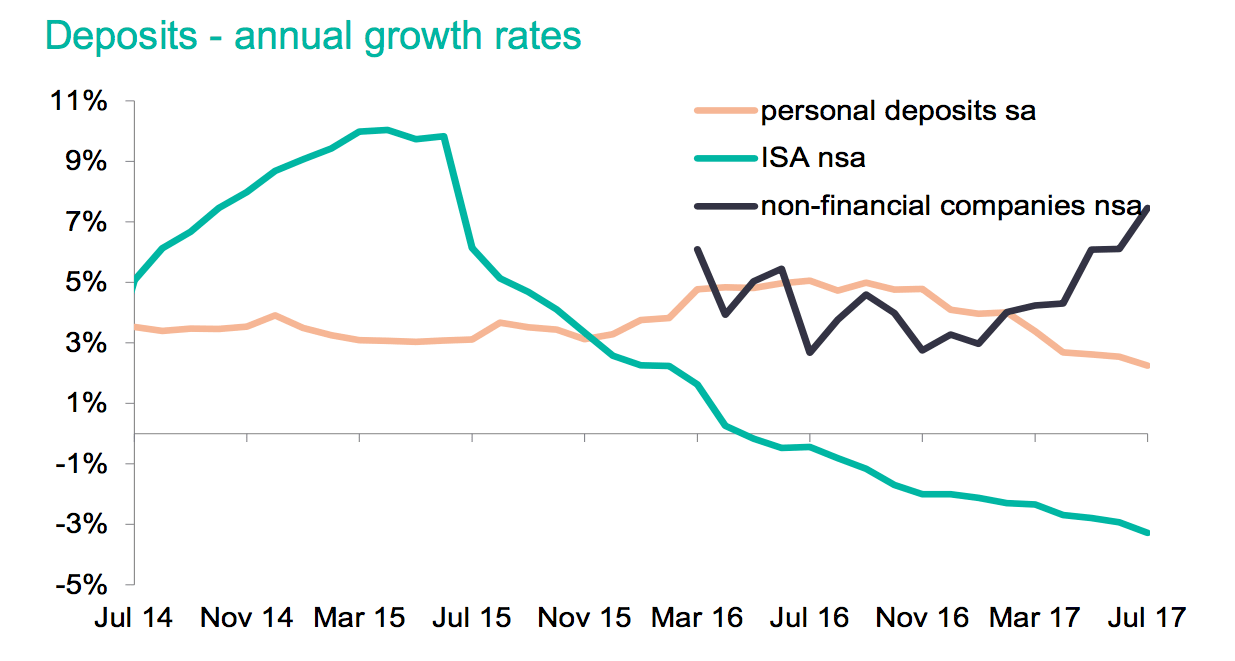

At the same time, savings have continued to decrease, with UK Finance once again revealing in a report from yesterday that the annual growth in personal deposits was only 2.3% in July, the lowest rate since May 2009.

Source: UK Finance, Statistical release on high street banking, August 24th 2017

Taken together, this means that the UK public are borrowing more and putting less away for a raining day, something which has resulted from the squeeze on living standards and the growth in inflation that's currently gripping the UK.

As the Bank of England have warned on numerous occasions now, the high level of debt means that not only are borrowers vulnerable to shocks to the economy (such as increasing employment), but that their lenders are increasingly vulnerable.

That's because, if an economic dip or recession were to hit Britain, lenders would suddenly find that an increased number of their debtors were unable to repay what they owed on their credit cards, leaving them - the lenders - massively out of pocket.

Disappearing deals

And since 0% introductory deals represent a "ticking time bomb" for the banks because of this, they've reportedly begun curtailing the number of such deals they offer.

For instance, according to Moneyfacts, the following reductions have taken place over the past six months:

| 6 Months Ago | Apr-17 | 3 Months Ago | Aug-17 | |

|---|---|---|---|---|

| Number of 0% introductory balance transfer deals | 126 | 125 | The same (125) | 119 |

| Average 0% introductory balance transfer term (days) | 669 | 651 | 659 | 645 |

| Average introductory balance transfer fee | 2.29% | 2.24% | 2.27% | 2.16% |

Source: Moneyfacts

Converted into specific examples, what such reductions mean is that customers looking for the longest possible 0% balance transfer deal will find that the 43-month credit cards from Halifax and MBNA are no longer available, while 42-month cards from Lloyds Bank and Sainsbury's Bank have also disappeared.

Instead, customers will have to make do with either a 43-month balance transfer card from Santander that charges a £3 monthly fee (their All in One card), or the 40-month Platinum Balance Transfer Barclayscard.

Growth rates and base rates

This may come as something of a disappointment to anyone looking for a really long 0% balance transfer period, yet a decrease in the number of introductory deals from 126 to 119 is hardly the most drastic reduction ever, with customers still able to take advantage of a wide choice of balance transfer cards.

Added to this, there's little question that 40- and 39-month 0% periods are still pretty long, and they still exceed the 36-month period Barclays offered when, in 2015, they became the first lender to offer a 0% balance transfer card in three years.

And what's interesting about this is that Barclays came out with their new card at a time when credit card debt was growing faster than it did in 2016 and in almost every month of 2017.

| Year | Growth rate in spending value | Growth rate in number of transactions |

|---|---|---|

| 2012 | 1.1% | 5.1% |

| 2013 | 4.4% | 7.5% |

| 2014 | 6.7% | 9.9% |

| 2015 | 6.4% | 12.4% |

| 2016 | 2.7% | 7.2% |

Source: UK Finance, Card Expenditure Statistics, 2017

In other words, credit card debt was growing faster in 2014 and 2015 than it has for most of 2016 and 2017, so it's unlikely both that a) banks genuinely are beginning a major clamp down on 0% deals and that b) if they are, they're doing so because of the recent growth in credit card spending.

Source: UK Finance, Statistical release on high street banking, August 24th 2017

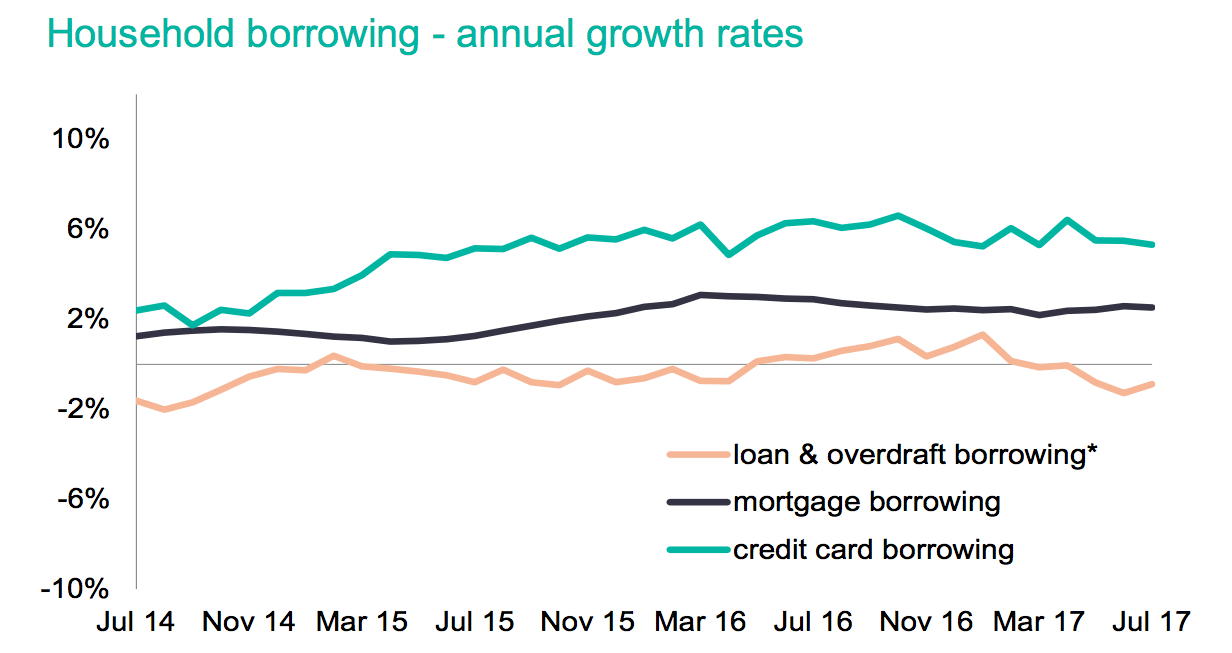

And as the graph above shows, the growth rate of credit card borrowing has been going up and down quite regularly in past months and years, underlining how it would be very difficult for banks to draw out a reliable medium or long term trend for credit card spending overall, especially given the instability of the UK economy.

All of which means that credit cardholders shouldn't worry that long 0% balance transfer and purchase deals are about to start becoming scarce. Then again, if the Bank of England finally deliver their long-awaited base rate increase - which many people expect by the end of the year - then this could be a very different story indeed.

We are independent of all of the products and services we compare.

We order our comparison tables by price or feature and never by referral revenue.

We donate at least 5% of our profits to charity, and we aim to be climate positive.

Latest News

26 October 2022

Cost of living showing worrying trends in affordability

16 June 2022

FCA warn lenders on cost of living difficulties