How to earn extra with your card

Can my card debt be cancelled?

Where to go for debt help

Are interest-free credit cards to blame for debt binge?

Credit: Treecha/Shutterstock.com

After having warned of rapidly growing household debt in November, the Bank's Financial Policy Committee (FPC) took the opportunity to issue another warning, stating that "the gradual extension of interest-free periods on credit card balance transfer offers" was one of the chief reasons for the fastest rate in consumer borrowing since 2005.

They also singled out "an increase in maximum loan limits in some parts of the

unsecured personal loan market," suggesting that lenders are putting themselves, their customers and the wider economy at risk by lowering their standards for awarding credit.

However, while the extending of interest-free and loan periods is certainly a factor in a deepening of competition among banks for customers, it certainly isn't the fundamental reason as to why people are choosing to go more into debt, with a squeezing of living standards among non-retired, working-age people likely to be a more important underlying factor.

Balance transfers

Relevant guides

This isn't to say that there hasn't been a growth in interest-free balance transfer credit cards recently, or that the interest-free period on them hasn't been growing on average.

In 2015 - when Barclays became the first bank to offer such a card since 2012 - the typical interest-free loan period was 36 months or less, meaning that a customer could transfer a balance from a previous credit card and not be charged any interest on her debts for as long as three years.

Now, some balance transfer cards are going beyond even this generous grace period, with Santander, Sainsbury's, MBNA, and many other lenders all offering interest-free periods that last for as many as 43 months.

That every bank is now offering such cards after a financial crisis-induced lull has caused the Bank of England (BoE) some concern, with the FPC once again noting in their meeting that consumer credit "reached an annual growth rate of 10.9% in November 2016 - the fastest rate of expansion since 2005."

More worryingly, they also noted that "the proportion of households with high consumer credit debt service ratios was broadly equivalent to that with high mortgage debt service ratios".

What this means is that, because of high interest rates and shorter repayment periods (compared to mortgages), people with credit card debt find it just as difficult to repay what they owe as all those homeowners whose mortgage debt currently makes up a hefty 102% of annual UK household income.

And more importantly for the FPC, such high "service ratios" present a risk to lenders, who may find that "the scale of losses on consumer credit books in an economic downturn [is] likely to be greater than that on mortgage lending."

They went on, adding, "For example, in the 2016 stress test, stressed impairments on UK consumer credit exposures totalled around £18.5bn, compared with £11.8bn for UK mortgages".

Economic imbalances

Useful Links

The best purchase credit cards

Balance transfer cards - who's the best?

Transfer cards for existing customers

Life or 0% - which saves more?

Balance transfer cards - who's the best?

Transfer cards for existing customers

Life or 0% - which saves more?

That said, while banks could certainly protect themselves from some exposure by shortening interest-free periods, it's not really balance transfer credit cards or low "underwriting" standards that are responsible for this risk.

Instead, it's the economic conditions that lead people to take out such cards, and that create an expanding yet fragile market that banks respond to by offering interest-free deals.

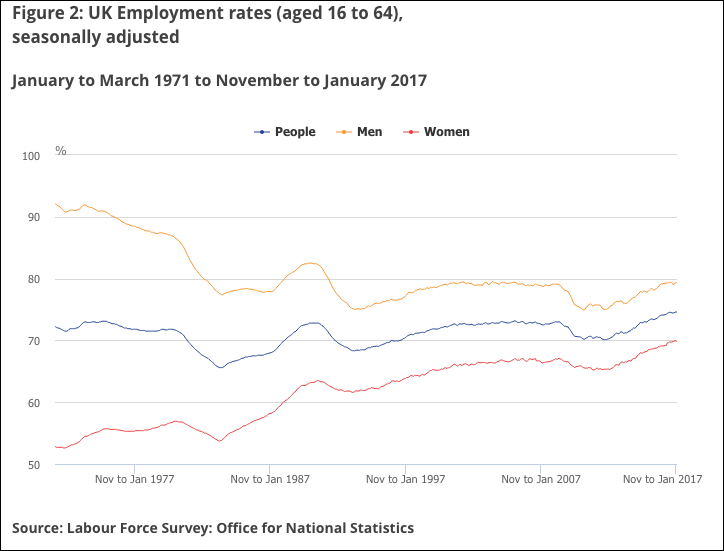

To begin with, since 2015 - when balance transfers started making their comeback - employment has hit record highs, with new peaks being successively scaled in February 2015, July 2016 and then once again this February.

At the moment, the employment rate stands at a seemingly healthy 74.6%, having grown by 0.5% between January 2016 and January 2017. Unfortunately, much of this growth has come from temporary and insecure working, with the number of people in zero-hour contracts growing (between December 2015 and December 2016) by 0.3% to 905,000 (2.8% of all people in employment).

Added to this, for those who are in regular full-time work, they've found that their incomes have actually shrunk since the financial crisis, while living costs and inflation have continued to climb, the latter hitting a high of 2.3% this February.

This is important, because in expanding employment while actually stretching working-age incomes, the economy has created the ripest possible conditions for a growth in consumer borrowing and balance transfer credit cards.

The squeezed incomes mean that more people want to borrow money to fill the gaps left by their frozen salaries, while the increased employment means that banks are more willing to lend them money, since they feel safe that an increasingly employed customer base will pay off their debts sooner or later.

This is the real reason why they've been willing to compete with each other and extend interest-free periods, and not because of any real recklessness or over-aggressive marketing on their part.

And this is something the Bank of England - and more particularly the Government - should bear in mind when seeking to address the alarming growth in household debt.

We are independent of all of the products and services we compare.

We order our comparison tables by price or feature and never by referral revenue.

We donate at least 5% of our profits to charity, and we aim to be climate positive.

Latest News

26 October 2022

Cost of living showing worrying trends in affordability

16 June 2022

FCA warn lenders on cost of living difficulties