118 118 Money want to know about your Facebook friends

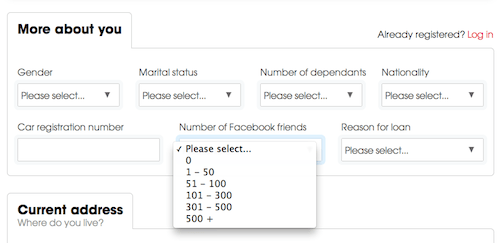

The lender, which is affiliated with the 118 118 directory service and targets applicants with poor credit histories, asks about Facebook early in the form, right alongside address details.

Although 118 118 Money, which launched in the UK last September, told us that they do not take the number of Facebook friends applicants have into account when deciding whether or how much to lend, they will "include this into future analytics to consider whether [Facebook information] allows them to make more informed lending decisions."

In other words, the lender is moving towards using information from Facebook to determine creditworthiness, as are many other loan providers.

Why lenders want your Facebook data

Credit: Choose.net screenshot taken 12/5/14.

Banks and other financial institutions have always tried to get a look at any and all types of information in order to ensure they see their investment returned.

Standard credit reports from the big reference agencies confirm addresses using the electoral roll, details of financial court judgements from court records and information on borrowing through information sharing with lenders.

Since social media activity is yet another well of information about individuals, it's no surprise that some lenders want to see that, too, especially when they're looking at applications from borrowers who have a limited amount of information with the standard sources above.

118 118 Money offers borrowers short term loans of £1,000 to £5,000 with repayments over one to two years. The firm's blurb claims that, "combining the power of analysis with deeper assessment by our experienced underwriters, 118 118 Money aims to make lending more available to hardworking, creditworthy consumers."

118 118 Money told us that they want to use Facebook information in order to "better understand customers and help to build a relationship with them" and added that, "using [information from social media] and real time bureau data could avoid pushing up the cost of borrowing to customers or denying affordable loans to many legitimate borrowers with less than perfect credit ratings."

In other words, the lender plans to use social media information to supplement standard credit rating information, particularly to indicate the likelihood of repayment or default.

Friending your lender

However, at this stage 118 118 Money are only asking their applicants about their Facebook friends to assess how useful this information could be.

Some other lenders are far further along: number of 'friends' is a pretty blunt measurement of a person's creditworthiness especially compared to the wealth of other information - liked pages, associations, frequency of type of updates - that could be found through direct access to applicants' profiles and linked to repayment behaviour.

Wonga, the payday lender that thinks of itself as a digital company, has previously encouraged users to connect their Facebook account to their Wonga application with the words "Facebook Connect helps us to know you better. This will improve your chances of being approved for a loan".

Agreeing installed an app which had access to a huge amount of Facebook data: birthday, home town, location, educational history, work history, relationship details and all that information shared by friends.

Like many other lenders, Wonga are proud of their proprietary system for sorting loan applicants and social media is just one of many things the company looks at when assessing applications.

A Wall Street Journal report on the use of social media data published last September confirmed that Wonga are not alone: US lender Moven as well as East European Kreitech are also using social information - from Twitter and Linkedin, as well as Facebook - to influence lending decisions.

No loans for luddites

It's clear from these companies successes that there are already a good deal of customers wiling to give access to their data, though it's unclear if everybody understands what connecting with Facebook really means.

As the world moves further and further into a digital reality, and privacy refuses itself to most people, a more concerning factor may not be the approval of some customers based on their Facebook friends.

Lack of a Facebook account may become akin to lack of a credit rating in the world lenders like Wonga and 118 118 Money appear to be headed towards.

Luddites, who do little or no social networking, may be refused loans simply because they are a mystery to the lender's systems.

We are independent of all of the products and services we compare.

We order our comparison tables by price or feature and never by referral revenue.

We donate at least 5% of our profits to charity, and we aim to be climate positive.

Latest News

26 October 2022

Cost of living showing worrying trends in affordability

16 June 2022

FCA warn lenders on cost of living difficulties