Best cash ISAs: more

Transfers: more

ISA or P2P: more

Banks gear up for new £15k Nisas

Credit: bangoland/Shutterstock.com

JUST a week after they were announced in the Budget, banks and building societies have started gearing up to offer 'new ISA' (Nisa) accounts.

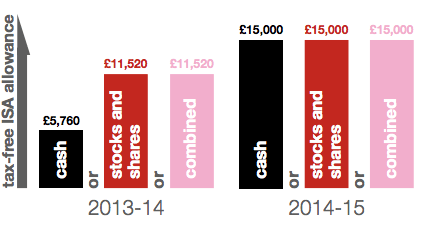

From July 1st, savers will be able to put away up to £15,000 in cash tax-free into a Nisa.

Currently, and up until the end of the tax year on April 5th, the cash ISA limit is £5,760.

New ISA rules. SOURCE: UK Treasury 2014.

It's a big bonus for those with money to put away tax free but leaves ISA providers with a four month grey area, which they're just starting to work out how to fill.

How ISAs will become nicer Nisas

Banks and building societies are likely concerned that people will hold off on opening savings accounts until they see how the Nisa market pans out, depriving them of savings at what is normally a busy time for new accounts.

- Now until April 5th: 2013-14 cash ISA limit of £5,760.

- April 6th to July 1st: 2014-15 cash ISA limit of £5,940.

- July 2nd onwards: Nisas introduced, all ISAs opened since April 6th become Nisas with a £15,000 cash limit.

Skipton Building Society have sought to reassure savers that opening an ISA won't lead them to miss out on Nisas.

Customers with their easy access accounts will be able to top up to the new £15,000 subscription limit during the rest of the tax year, the ISA provider said this week.

More practically, many of the top cash ISAs at the moment have fixed rates and fixed windows for savers to fund the accounts.

In this case, it's likely that many will follow the example of Halifax, which announced today that it will triple its cash ISA 'transfer in' window from 60 to 180 days.

More on ISAs

Again, that'll allow savers to benefit from putting money into a tax free account from the beginning of the tax year and still be able to top up to the £15,000 limit when it becomes available in July.

Another new challenge for the banks will be allowing customers to move money they currently have in stocks and shares ISA to a cash Nisa.

According to a poll released by Nationwide Building Society last week, 12% of over 45s with a stocks and shares ISA wanted to move their money to a cash ISA, even though they couldn't have done so under the old ISA rules.

40% of those polled that wanted to move their money out of investments thought it'd be safer in cash, Nationwide said, while 31% thought that a cash ISA would give them more flexibility.

Are savers better off?

The move to Nisas was unexpected but both the increase in the tax free allowance and the increased flexibility for savers was widely praised as a big win for savers.

However, as many have pointed out, an increase in the limit primarily benefits high income savers who will now be able to avoid tax on all their savings.

The Institute for Public Policy Research think tank estimates that someone saving 20% of their disposable income would need to earn about £125,000 to put away the whole £15,000 yearly limit. The average salary is £26,500.

The new ISAs seem to bring few benefits to those unable to meet the current annual limit and they certainly don't do anything for the millions of people who struggle to put anything away at all.

Having said that, however, ISAs are well loved among people with middle incomes. In 2010-11, according to HMRC, most ISA holders had annual incomes between £10,000 and £19,999 and, according to the Budget speech, 75% of those who hit the cash ISA limit are basic rate taxpayers.

And there are some benefits to a bigger limit for those with less to put away.

Lower income groups have a strong preference for saving in cash ISAs, rather than in stocks and shares, according to HMRC statistics, so the new more flexible form will give them more room to save where previously the need to invest might have put them off.

Another problem: interest rates

Based on the current best buy rates, savers could earn up to about £250 more in interest a year by investing the new full limit.

But that's based on the very best fixed rate accounts which will include plenty of restrictions and, even then, aren't offering the returns we've seen in previous years.

The best buy with easy access currently pays just 1.65% AER, there are current accounts that beat that.

It's also worth bearing in mind that these are today's rate. There's no way of knowing how these changes will affect the interest rates on offer later in the year.

Some critics think that, as savers with a lot of money to put away become more motivated to save in cash, banks will have even less incentive to offer good interest rates.

We are independent of all of the products and services we compare.

We order our comparison tables by price or feature and never by referral revenue.

We donate at least 5% of our profits to charity, and we aim to be climate positive.

Latest News

26 October 2022

Cost of living showing worrying trends in affordability

16 June 2022

FCA warn lenders on cost of living difficulties