How they work

Different loan choices

Debt help

Payday costs to be capped at 0.8% a day

Credit: Sam72/Shutterstock.com

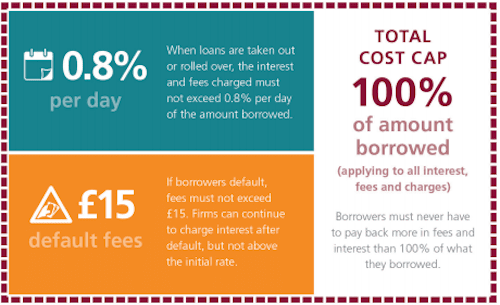

Under the proposals, payday customers cannot be charged more than 100% of the amount they initially borrowed.

In order to limit the amount due further, interest rates could be capped at 0.8% every day and default fees could be capped at £15.

So, for example, someone taking a payday loan of £100 repaid over 30 days would have to repay, at most, £200, broken down into the following charges:

- £24 interest the standard charge for taking the loan.

- £15 in fees maximum, if the loan is overdue.

- £61 maximum, in default interest if the loan is overdue. This amount would only be charged if the loan went unpaid for 67 days.

SOURCE: FCA proposals for a price cap consultation [pdf] 15/07/14.

The FCA say they hope this mix of different caps will make payday loans easier to understand, radically reduce the cost for people that do choose to take them and protect borrowers who get into difficulty.

"For the many people that struggle to repay their payday loans every year this is a giant leap forward," Martin Wheatley, the FCA's chief executive officer, said.

Shrinking payday

The impact of these proposals will be significant.

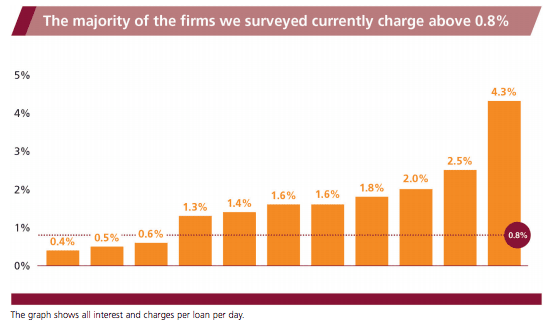

The daily interest rate cap alone will force the vast majority of payday lenders to lower their rates, as you can see below.

SOURCE: FCA proposals for a price cap consultation [pdf] 15/07/14.

In terms of actual cash savings, the FCA estimate that these proposals will save payday customers £250 million a year in standard interest, default fees and other charges.

A payday loan customer who pays back on time will pay £14 less, on average, than they'd pay today.

These limits will shrink the payday market significantly. Firms will lose about 40% of their total annual revenues and it's likely that many will quit the market. Many have already left following tougher FCA regulation or specific enforcement action.

Fuelling illegal lending

But Wheatley acknowledged that not everybody will agree with today's plan. "There have been many strong and competing views to take into account," he said.

Payday help

In particular, this cap is open to the same charge that all previous attempts to cap payday costs have faced: it will mean that less people can borrow, and that could fuel an increase in more dangerous illegal lending.

The FCA acknowledge that today's proposals will mean that many people who can take these loans now soon won't be able to. About 11% of people (or 160,000 people a year) who would otherwise be able to access get high cost credit would no longer be able to get loans.

However, they say, it is unlikely that this 11% will turn to illegal lenders instead.

Less than 5% of payday customers who are turned down for a payday loan say they'd even considered going to an illegal lender, according to FCA research.

Relying on people to tell the truth about doing something illegal doesn't make for the most accurate research but the regulator is clearly weighing the possibility of black market lending against the benefit of turning people in debt away from payday altogether.

The financial records of payday customers who struggle to repay show that most have no savings and a number of outstanding debts, the FCA say.

Borrowing elsewhere or seeking out debt advice is likely to be much more beneficial than taking a payday loan.

We are independent of all of the products and services we compare.

We order our comparison tables by price or feature and never by referral revenue.

We donate at least 5% of our profits to charity, and we aim to be climate positive.

Latest News

26 October 2022

Cost of living showing worrying trends in affordability

16 June 2022

FCA warn lenders on cost of living difficulties