Top paying accounts here

Regular savers here

On ISA vs P2P here

FCA joins fight against zombie accounts

Credit: Piotr Swat/Shutterstock.com

The report highlights the issue of "zombie accounts" - those opened some years ago and now earning next to nothing in interest.

It also suggests that many people with savings know they're getting a bad deal but think it's too much hassle to switch, and that there isn't much to be gained from doing so.

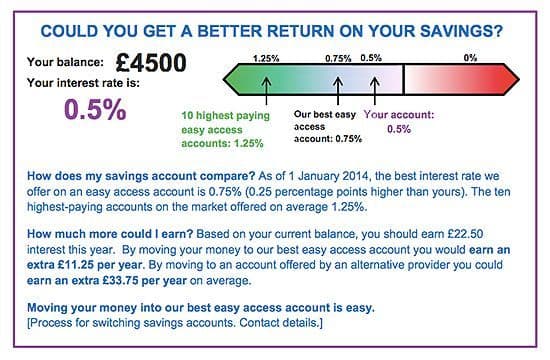

To that end, as well as adding to calls for a shake-up in the savings sector, the FCA has outlined some possible solutions, including getting providers to display their lowest rates much more prominently.

Zombies and legacies

How to save more

Some 93% of adults in the UK have some kind of cash savings account, with around £700 billion stashed away nationwide.

Just over half of that, around £354 billion, is stored in easy-access accounts which tend to pay lower interest - and about a third of these accounts were opened more than five years ago.

That means they're likely to be 'zombie accounts' - those that may have offered reasonable interest rates when they were opened but have seen the rate decline over time to the point where they're earning less than 0.5% - and in some cases as low as 0.05%.

In fact, the FCA say that in 2013 around £160 billion was stored in easy access accounts that earned equal to or less than 0.5%.

A similar but slightly different issue is that of legacy accounts.

To add to the 350 different savings products on the market at the moment, the FCA estimates there are more than 1,000 different types no longer offered to new customers but still active - in the sense that they have money in them.

Anyone whose savings account is more than a year or two old is likely to find it's become a legacy product - and depending on its age and terms and conditions, it could be well on its way to becoming a zombie.

If that sounds overly dramatic, bear in mind research from Which? that suggests more than 80% of us don't know what the interest rate on their savings is, while a quarter of those who've snagged themselves a bonus rate don't know when it will end.

The result is that as a nation we're losing out on an estimated £4.3 billion a year.

Small may be beautiful

The issue of easy access affects the level of interest on offer in another way - the biggest providers, with a branch in most towns and a solid online presence, naturally scoop up more custom than smaller or more regional institutions.

While the sense of familiarity may be comforting, that's about all the benefit many savers will get. The biggest banks and building societies tend to pay much lower rates of interest than their smaller competition.

It's partly because smaller and newer providers need to keep attracting custom to stay in business, but it's also a conscious move on the part of some of the larger banks.

They don't want to attract "rate chasers" - those savers who move their money more frequently, sticking around just long enough to make the most of a good deal but not providing long term (zombie) funds for the banks.

"It's not worth it"

Meanwhile many people say there isn't much to be gained by switching accounts: some people cited too little difference in the rates on offer, while others said they had too little saved for any change to make a difference.

Unsurprisingly, the more people have in their accounts the less likely they are to think this - but the FCA reckons that accounts containing more than £5,000 make up at least £145 billion of the money kept in easy access zombie accounts.

Again, the big banks win in terms of convenience - about a fifth of people say they wouldn't switch because they like the simplicity of having all their accounts in one place.

But unless someone also has outstanding balances on credit cards or other debt, there's almost always some way of making even the smallest rainy day fund work a bit harder, as we discuss here.

Some of the suggested fixes

There's evidence that telling people when their interest rates are due to change does make a difference - and not always to the detriment of the current provider.

The FCA says that while those reminded before the rate changed tended to move to another firm or type of account, those told afterwards were more likely to opt for a similar account with the same institution.

Opening new accounts should be made easier and quicker, with a shorter target time for the transfer of cash ISAs, and more widespread use of electronic anti-fraud identification checks.

The regulator also wants financial providers to prominently display the interest rate of their lowest paying savings account both online and in branch.

SOURCE: FCA Cash savings market study report 01/2015

The idea is that by doing this, it would alert customers to the rate they may well be getting themselves - and put pressure on the providers to improve their products.

We are independent of all of the products and services we compare.

We order our comparison tables by price or feature and never by referral revenue.

We donate at least 5% of our profits to charity, and we aim to be climate positive.

Latest News

26 October 2022

Cost of living showing worrying trends in affordability

16 June 2022

FCA warn lenders on cost of living difficulties