Auto-enrolment pension charges capped at 0.75%

Over the next 10 years, the Department for Work and Pensions (DWP) say the cap will make pension pots £200 million bigger.

But not all pension charges will be capped. Notably transaction charges - those from buying, selling, lending or borrowing investments - are excluded from the rules.

However the Financial Conduct Authority (FCA) will introduce reporting requirements for both administration and transaction charges this autumn, hoping to improve transparency in the industry.

Big difference

Director of strategy and competition at the FCA, Christopher Woolard, said: "It is important that those saving into workplace pension schemes get value for money and this is especially true for those who are not playing an active role in deciding where their money is invested."

The cap for auto-enrolment pensions comes into effect on 6 April 2015 together with additional bans. For some, it will mean a big difference in savings.

The DWP say a person earning an average salary and currently paying 1.5% charges could save an extra £100,000 over their working life.

Pension firms will be banned from paying or receiving consultancy charges and paying commission for advice, unless agreed to by scheme members.

And charging more when people decide to defer their pensions will also be banned; overall charges must be the same regardless of whether someone is or isn't contributing.

Weak competition

Highlighting just how murky pension charges are, it's unknown how many people are currently charged above the cap.

Best estimates come from a study published by the Office of Fair Trading (OFT) back in 2013.

The study looked at annual management charges (AMCs), which include administration charges.

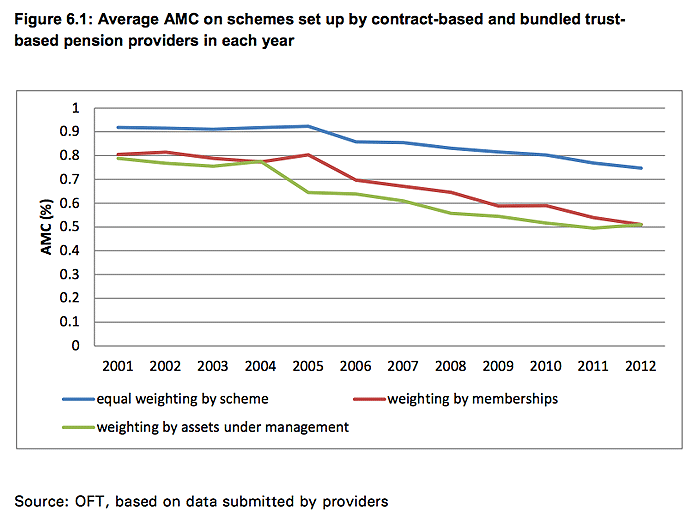

In 2012, AMCs were on average 0.51% - well below the new cap. And as the graph below shows, these decreased from 2001 to 2012.

SOURCE: OFT, Defined contribution workplace pension market study, September 2013. Available here [pdf]

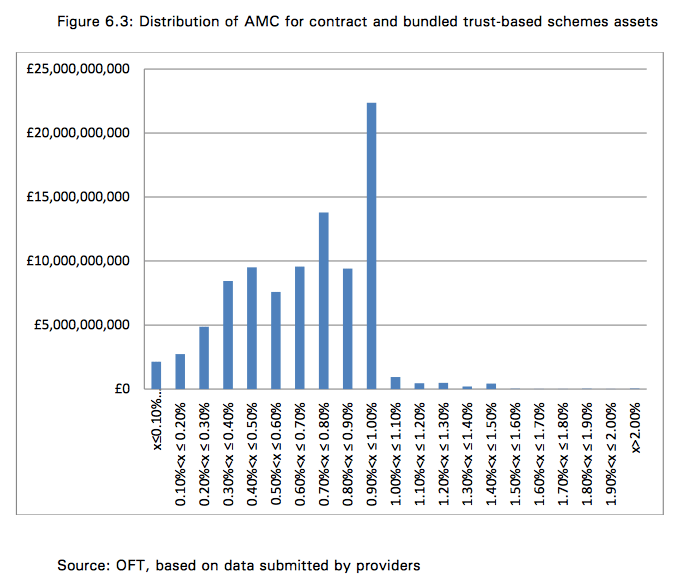

But this low average is because there is wide variation between the lowest and highest charging firms - ranging from 0.05% to 2.3% in 2012.

Importantly, nearly a quarter of firms charged 0.9% as can be seen in the graph below.

SOURCE: OFT, Defined contribution workplace pension market study, September 2013.

The OFT say the market is "one of the weakest" they've analysed, with little reason for pension scheme providers to give people a good deal.

By introducing a cap for auto-enrolment pensions, the FCA hope competition and value for money will improve.

"Dark corners"

Pension scheme providers will have to report their administration charges each year after the pension cap is introduced in April.

But the OFT highlights the difficulty of comparing charges between firms; each calculates and defines its charges differently.

As a worst-case scenario, this practice may be hiding mis-charging.

The FCA and DWP are unconvinced pension charges are clear or comparable across the industry.

So they're consulting with the industry on how administration and transaction charges are defined.

They'll then introduce a standardised system for reporting charges and make it clear who should get that information.

Giving employees such detailed information has been met with some opposition from the industry, however the FCA and DWP see it as essential.

Minister for Pensions, Steve Webb said: "There is a fear that the dark corners of the investment and pensions industry hold some nasty surprises. We have a duty to throw light for the first time on potential hidden charges - and restore faith and fairness in British pensions."

While current focus is on charges for auto-enrolment schemes, the FCA is considering widening the scope to include other pension schemes.

We are independent of all of the products and services we compare.

We order our comparison tables by price or feature and never by referral revenue.

We donate at least 5% of our profits to charity, and we aim to be climate positive.

Latest News

26 October 2022

Cost of living showing worrying trends in affordability

16 June 2022

FCA warn lenders on cost of living difficulties